I have several money-saving habits. It’s hard to estimate exactly how much money each of those habits has brought me. But hands down, the most impactful is:

I have several money-saving habits. It’s hard to estimate exactly how much money each of those habits has brought me. But hands down, the most impactful is:

- Paying Myself First

For years, I struggled with saving money. I had been saving a portion of my salary only to spend money on some substantial item like repairing my car after I drove straight into a tree; or something lavish like gambling on the stock market.

I had been earning good money—but I had no support from my family. I had no assets at the beginning and a family of five to support

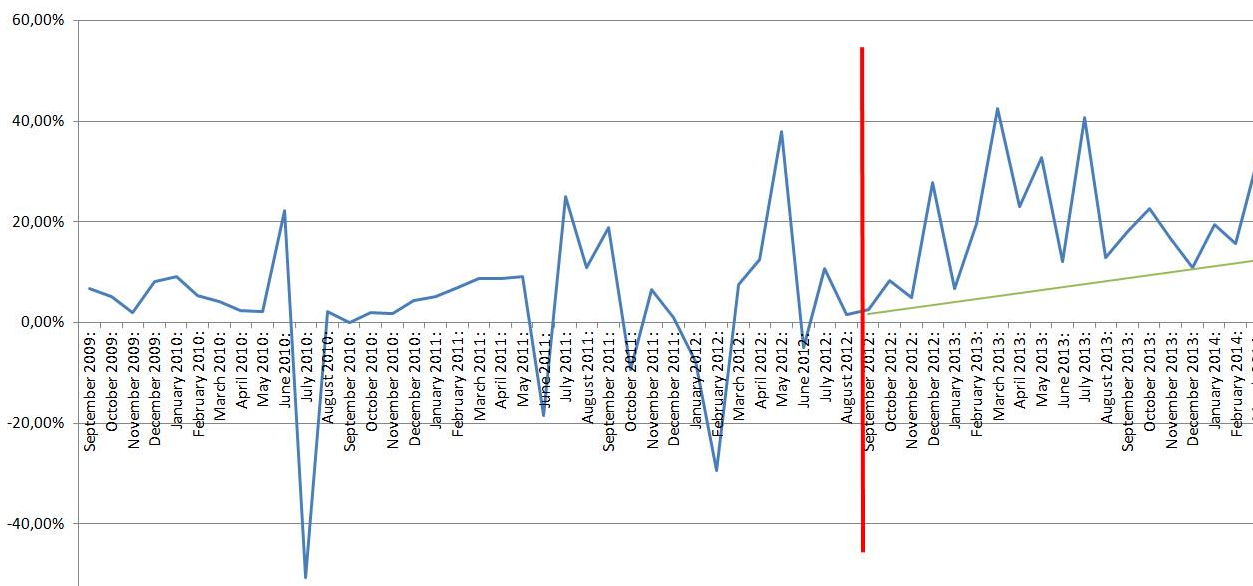

My saving ratio was hoovering about 3-4% point. Then I read “Start Over, Finish Rich” by David Bach and got one main takeaway from it: pay yourself first.

The idea seemed a bit preposterous, our budget was tight and we had no leeway to put away a significant chunk of salary. What difference would have made saving money at the beginning of the month and not at the end of it, from leftovers?

It did all the difference.

(my saving ratio over time)

(my saving ratio over time)

In a few months’ time, my saving ratio skyrocketed to about 20%. Yet again I spent all of my savings when we bought our first house in 2014. For several months, we were almost as poor as during my time as a student—having two kids and on welfare. We survived on stipends, and student loans as our main sources of income.

But I rebuilt my savings… and spent them once again on the house renovation.  That was at the beginning of 2016.

That was at the beginning of 2016.

Still, I was able to save for those extraordinary expenses thanks to the “pay yourself first” rule.

I estimate that thanks to the difference between my previous saving ratio and the current one—plus the fact that my income grew by about 90% in the last few years—I ended up with equivalent of my 14 salaries in my pocket. I spent about 10 of them, but I could spent them in bulk on expansive things that improved quality of our life; not on trivia.

The Other Six Habits

- No Addictions.

I don’t smoke; don’t drink alcohol; and never did recreational drugs. Those “habits” can consume a large chunk of your income.

The fact is, I’m no saint and I actually have a few “light addictions.”

I spent a small fortune on books and I have a hopeless sweet tooth. The last addiction I mentioned has downsized and became manageable in the last few years.

- Paying With Cash.

I was about 30 years old when I paid with a debit card for the first time in my life.

Good for me.

Paying with a card can lull you into thinking that the money is not real. But the bills are real as well as the balances you have to pay.

Till this day, I prefer to pay with cash and I manually register every automatic/digital payment on an Excel sheet. It works wonders with your awareness—of where your money actually goes.

- Not Eating Out.

I have family of five to feed. It’s much cheaper (and healthier) to buy ingredients and cook your own meals. In the last 5 five years, I’ve ate out maybe a couple dozen times—most of them when on delegation away from home.

- No Impulse Buying.

Alright—let’s be honest—I do very little impulse buying although I’m not completely immune to the shiny promises of marketing.

But I’m totally not interested in brands and sometimes it works against me. I’ve bought the cheapest laptop in the store and I discovered it is absurdly slow. I have a lot of opportunities to practice my patience with it.

But 99% of time, it serves me well. I bought an old Mazda 626 about 10 years ago. I put into it almost double the initial price (half of which after that accident with a tree). But that’s still much less than half the price of a new car and I know quite a lot of folks who exchange a car every few years. That Mazda is a small fortune “saved”.

I don’t follow trends and I don’t chase shiny objects. I buy new items when I need them; not when I want them.

- Tracking All Expenses.

I’m doing my best to register every single cent that’s going out of my pocket. I’ve tracked them in an Excel sheet since November 2012. I have quite a history in that file now.

Tracking sharpens your awareness. If you track your spending, it’s much harder to be ‘blissfully’ unaware how you spend your money and you think twice before wasting your money on trivial things.

- Saving the Excess.

In 2015, I changed jobs and got a salary hike of 35%. I kept my expenses at the same level but did not dedicate all of it to savings.

I didn’t dedicate even a dime of it to pay bills or buy food. I spent a bit more on charity—saved 30%—and invested 20% into my business.

I used only about 40% of that additional increase on consumption, but not for trivial things. I was able to afford to buy my wife a gold ring, send my kids to summer camp, purchase a computer and four bikes.

I do the same with my royalties. I treat this income as additional to my base income.

I save it—invest it—or spend it bigger items like a mortgage contribution, buying a second car, or house renovation. I intend to do that with every additional dollar till I become financially independent.

What are your money-saving habits?

hentai,

xporn,

Phim sex,

porno,

Argentine Vs Maroc,

What Were Kleenex Tissues Originally Used For,

Next Boxing Fight,

Pork Leg Cooking Times,

Wave Racer,

Skillsjhare,

Aus Racing Results,

Credit One Bank Activate New Card,

Is It Better To Pay Credit Card Before Statement,

Ncl Trip Insurance,

Hi, I am new here and find these financial habits really useful and I can use some to start building my own financial wealth. Eating out is really one big burner for me, and I am glad I have put a stop to it already. Thanks for the article.

You’re welcome Jimmy. Thanks for stopping by.